Here Is the $13 Billion Federal Case Against JPMorgan That Jamie Dimon Doesn’t Want You to See

President Barack Obama was swept into office in the wake of an unprecedented financial collapse initiated by unscrupulous banks, but his Department of Justice did precious little to actually punish the executives behind it. Obama’s federal prosecutors made almost no attempts to hold anyone criminally responsible, and they settled civil cases quietly, without the unpleasantness and embarrassing details of protracted litigation.

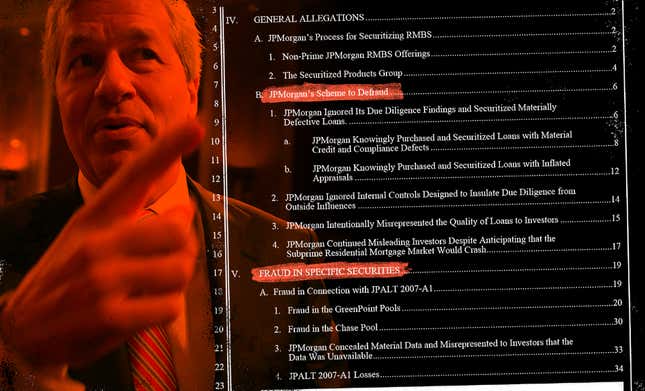

What would an open prosecution of bank malfeasance have looked like? In 2013, the U.S. attorney’s office for the Eastern District of California drafted an extensive civil complaint against JPMorgan Chase, describing a damning array of alleged financial fraud violations that had led to the 2008 meltdown. Rather than formally filing that complaint, though, the Obama administration used it to convince the bank to agree to pay a $13 billion settlement. After the feds and JPMorgan Chase had reached their deal, the government sought to bury the specifics of the complaint—blocking it from being disclosed in open court or through the Freedom of Information Act.

The concealment lasted until earlier this month, when Vanity Fair correspondent William D. Cohan reported the details of the complaint’s allegations, and the tortured history of the government’s—and JPMorgan CEO Jamie Dimon’s—efforts to keep them secret. The complaint had recently been unsealed in the course of a lawsuit filed by the First Amendment attorney Dan Novack. Cohan’s piece quoted from the draft complaint at length, but did not include the actual 92-page document.

Had it been filed, the complaint would have targeted JPMorgan as an institution, not individual employees. Nonetheless, the document details a litany of alleged misdeeds committed by the bank’s analysts and underwriters who had been tasked with creating, auditing, and selling mortgage-backed securities, the arcane financial instrument that devastated the global economy in 2008. Novack gave Splinter a copy, and we are publishing it here for the first time.

But even though the cat is finally out of the bag about the government’s evidence against JPMorgan Chase—four years later and under a new president—the Department of Justice still took pains to keep Jamie Dimon’s secrets. Twenty-one whole pages are completely blacked out, under an exemption to the Freedom of Information Act that protects information that may “interfere with [law] enforcement proceedings.”

It’s hard to see how the redacted material, if revealed, could interfere with any law enforcement actions. The government’s civil enforcement efforts apparently wrapped up in 2013, with the Justice Department’s announcement of the $13 billion settlement. And although that announcement noted that the agreement “does not absolve JPMorgan or its employees from facing any possible criminal charges,” most, if not all, of the events in the draft complaint occurred ten years ago, which would put them beyond the criminal statute of limitations.

The relevant law, the Financial Institutions Reform, Recover, and Enforcement Act, allows the federal government to seek civil penalties against firms for violations of certain criminal laws relating to the finance industry. Those laws usually have a statute of limitations of five years, but under FIRREA, the statute of limitations lengthens to ten years. The draft complaint repeatedly emphasizes that the Department of Justice looked at JPMorgan’s conduct “from 2005 to 2007,” which means that any such action would have to be launched in the next three months in order to stay within the statute of limitations.

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-