The American Economy Is Shockingly Dependent on AI

Photo by Stephen Brashear/Getty Images

Despite the world-historic amount of hot air coming from corporate America’s AI obsession, there is something happening in our physical reality beneath all this hype around chatbots that lie to you: a firehose of spending on AI infrastructure. Alphabet, Google, Amazon and Meta will spend almost $400 billion this year on capital expenditures (capex) like new data centers, more than the European Union spent on defense last year. McKinsey estimated that total AI capex will be $6.7 trillion by 2030. Famed tech founder Paul Kedrosky wrote that “AI capex is so big that it’s affecting economic statistics, boosting the economy, and beginning to approach the railroad boom.”

“The labor market might be softening. Housing and construction activity remain muted due to high mortgage rates. Tariffs could slow consumer spending,” continued Kedorsky. “Yet the biggest, most important companies in the stock market are pot-committed and continue to spend like your drunk friend in Vegas who just went to the ATM for the third time before midnight.”

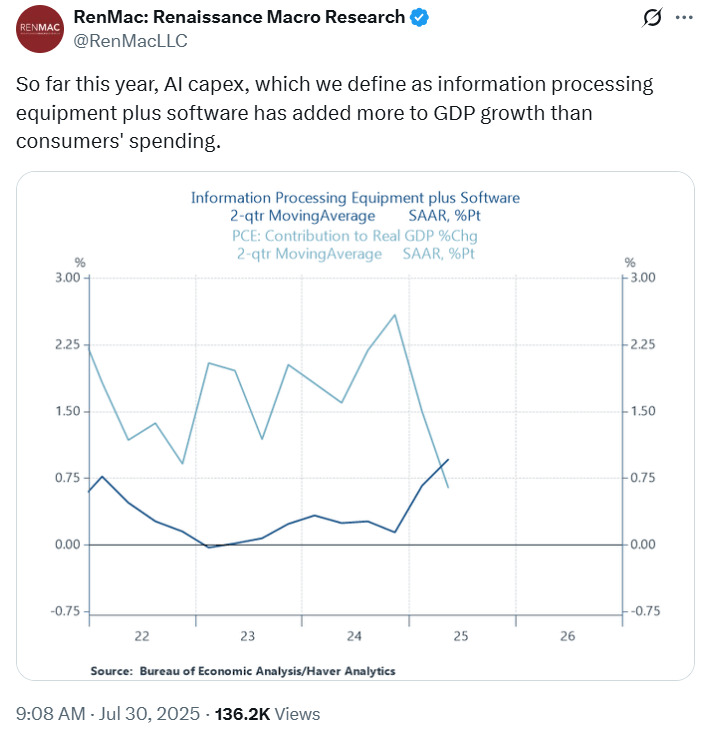

AI capex is so important it now surpasses the engine of the American economy, consumer spending, which typically comprises about 70 percent of GDP.

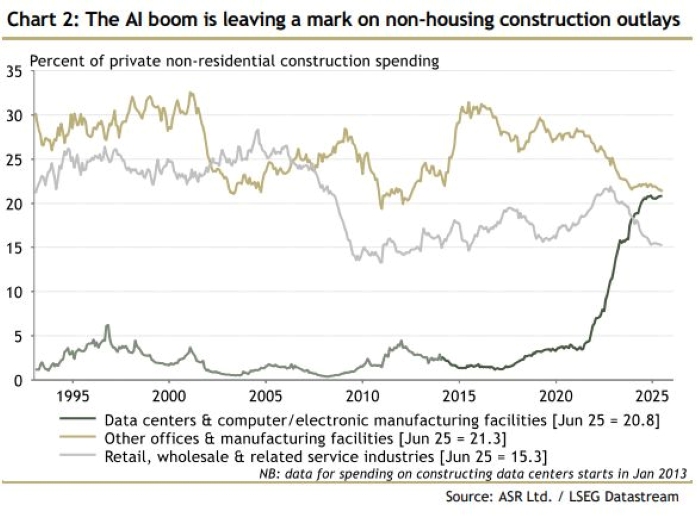

We now spend more on datacenters and such than we do on retail, wholesale and related service industries.

AI capex is the most important economic driver in America today. Jason Thomas of the investment firm Carlyle estimated that AI capex was responsible for a third of America’s second quarter economic growth. Without it, we would have a slowing economy defined by Trump’s trade war’s depressed demand. The new ISM manufacturing survey today came in below expectations at 50.1, implied a 4 percent inflation rate, and sits about as low in expansion territory as it gets before it flips into contraction (49.9). These charts are what creeping stagflation looks like.

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-