Bitcoin Is Falling Hard, And One Psycho Has the Power to Nuke It Straight to Hell

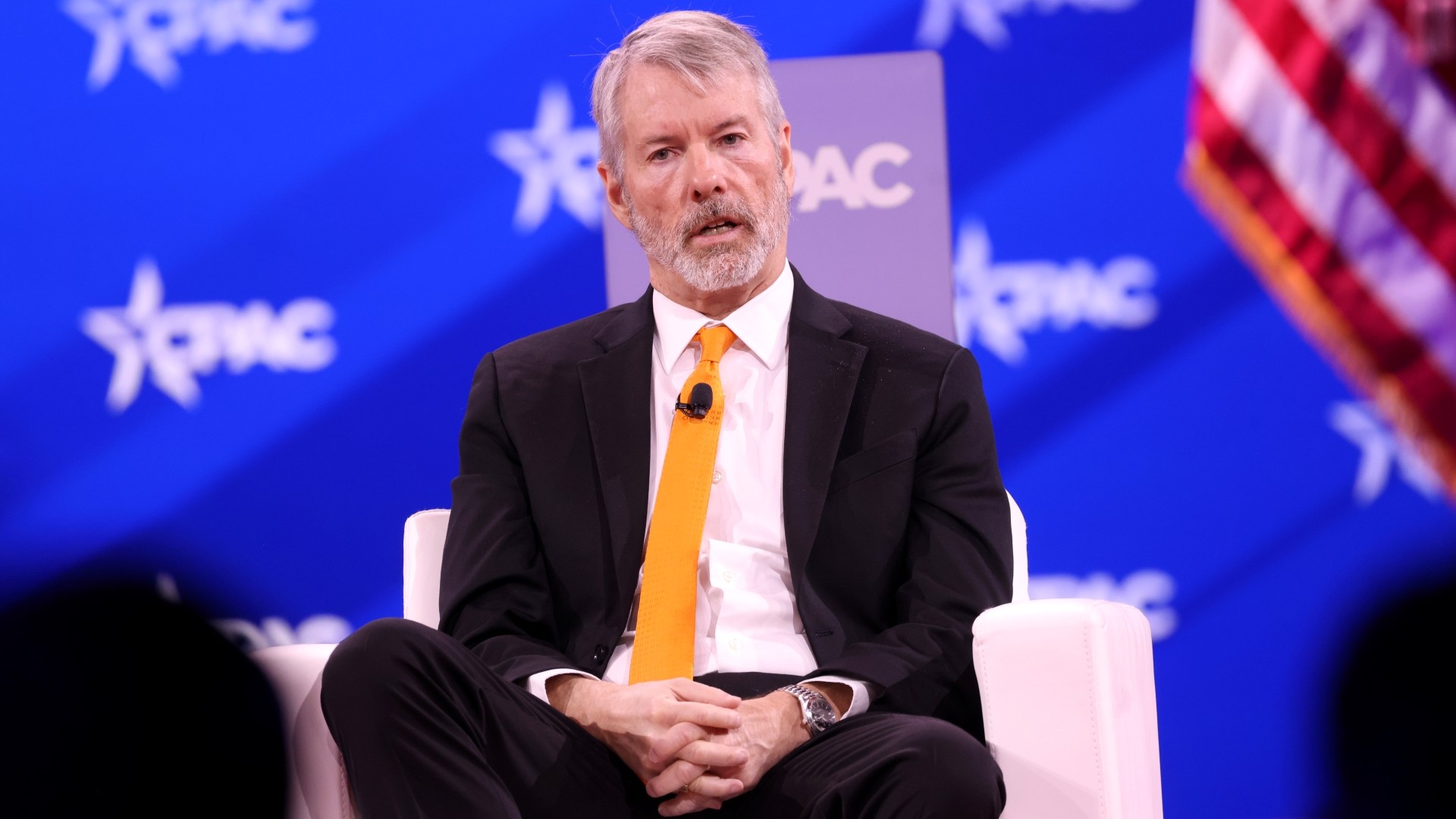

Photo by Gage Skidmore/Wikimedia Commons

The crypto bull run of 2024 to 2025 may be over, as Bitcoin is down 30 percent off its all-time high as I write this, a drawdown sparked entirely by a Friday Trump post that led to the largest leverage wipeout in crypto’s history that he TACO’d on by Sunday before the grown-up markets opened. So far this looks like a typical crypto cycle where it went higher than people expected, and is currently pulling back more than people expected. It’s not totally over for the bull run yet, but the fat lady is absolutely warming up to sing the final song of this crypto cycle and the bulls must rally to stop her soon, or else the selling momentum will lead Bitcoin to do what it always does and fall off a cliff.

The biggest threat to Bitcoin may actually have little to do with Bitcoin, and everything to do with one of the preeminent Bitcoin psychos, Microstrategy CEO Michael Saylor. He pivoted his business that doesn’t make much money into a Bitcoin treasury to try to turn his company’s fortunes around, and it turned him into the celebrity spokesperson for Bitcoin as he made increasingly unhinged up only promises. It’s worked pretty well up to this point for reasons that do not apply anymore, and now Saylor may be fucked.

Microstrategy owns a staggering 649,870 Bitcoins. At the current price of around $89,000, that’s $57.8 billion in Bitcoin for a company whose current market capitalization is $53.53 billion. You don’t need to be a math whiz to know that those two figures don’t look great next to each other. The market values Microstrategy’s Bitcoin holdings far more than it values the company itself.

I have written before about my own crypto adventures making then losing over a million dollars, and I did it the way all crypto people do it: leveraging their crypto holdings. If you own $100 worth of Bitcoin and use it as collateral to take out $30 in debt to buy more Bitcoin, you now have $130 in Bitcoin and $30 in debt. But if the value of Bitcoin falls in half, you now have $65 in Bitcoin while you still have $30 in dollar-denominated debt. If it falls far enough, your Bitcoin is automatically sold to cover your debt. Microstrategy has taken this leverage strategy to a very complex place, and it’s not as straightforward as a BTC crash would lead to them become forced sellers like I nearly was, but it is a leveraged strategy and they are very obviously the Sword of Damocles hovering over the entire crypto market.

Before the days of Bitcoin ETFs that anyone can put in their 401k, Microstraegy (MSTR) pivoted to a pretty clever model. There are all sorts of rules and regulations around financial institutions that do not allow them to buy Bitcoin directly, and so Microstrategy bought Bitcoin to give these financial institutions exposure to Bitcoin in a way that still kept them within their financial rulebook. Now that any old shlub can buy IBIT and get direct Bitcoin exposure and not this bank shot through a company that doesn’t make much money, it is far less clear what Microstrategy’s value proposition is these days outside of Saylor being Bitcoin’s preeminent hybebeast. They are just a Bitcoin treasury the same way that Gamestop and countless others are. Saylor isn’t special anymore and neither is the Bitcoin treasury model.

So what the fuck is Michael Saylor’s plan for Microstrategy now?

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-