Trump’s Trade War and Elon’s Coup Mean It’s Time to Learn About Inverted Yield Curves Again

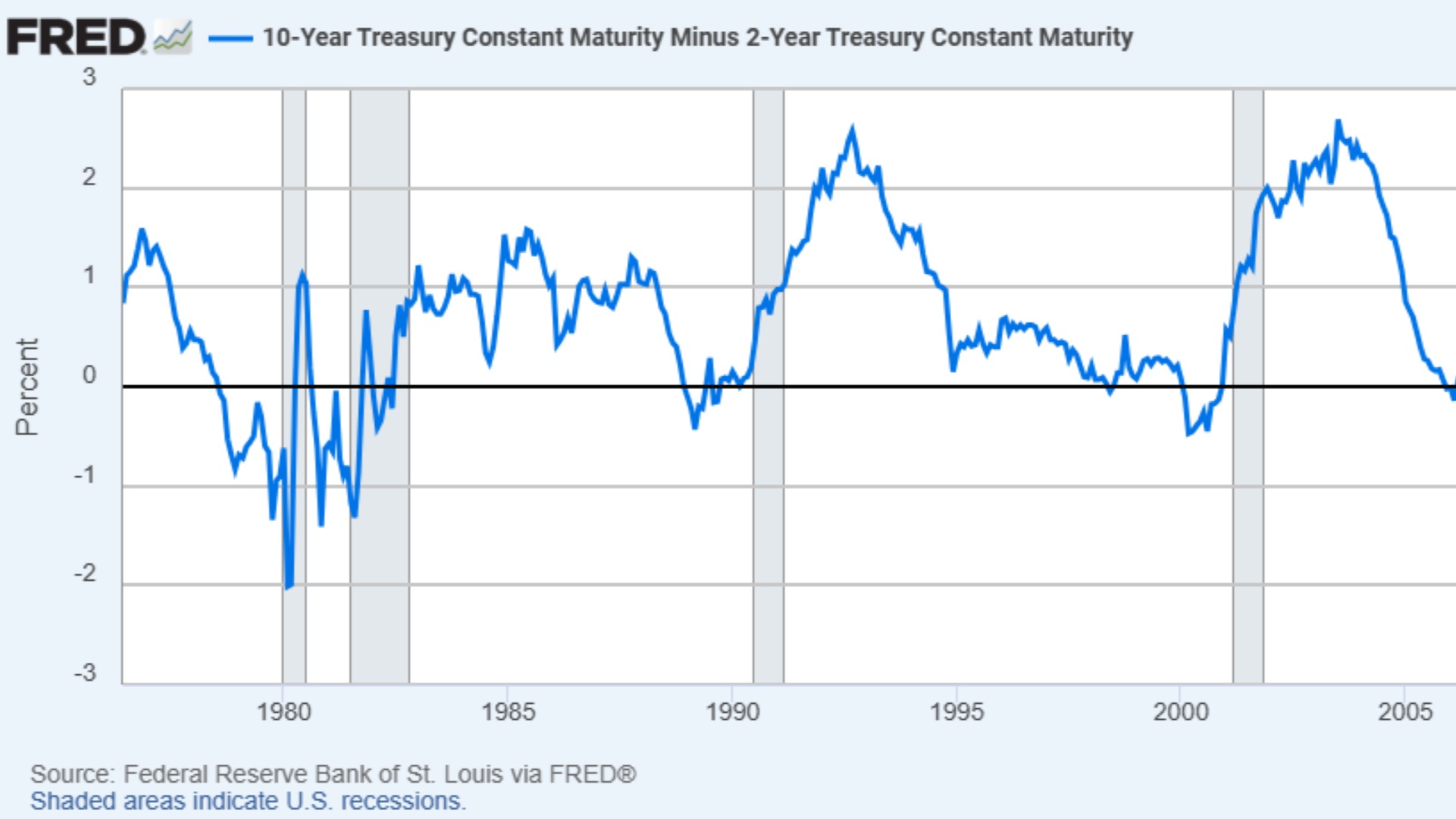

Photo by FRED

Last week was a big week for markets, as the trade war that everyone has been warning about has finally arrived. Despite what some of our most epic posters might tell you, the trade war is not off (the China tariffs are still on despite the 30 day delays for the ones on Canada and Mexico) and that was not a successful bluff by Trump to get Canada to do what it already pledged to do, and I can prove it with math.

The largest, most liquid market in the world spent last week sending the biggest, scariest warning signal it can: an inverted yield curve.

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-