A More Detailed Look at How Trump and AI Could Crash the Economy

Photo by The White House

Back at the start of this tariff madness in February, when you could see the outline of a shitshow through the haze, I wrote a generic “what Trump and Elon’s economic crash could look like” article. While I would have lost my entire April salary on my bet of the timing of the poor jobs report, I wasn’t exactly directionally wrong given that abnormally large downward revisions to jobs reports were the reason why Trump recently fired the head of the Bureau of Labor Statistics (BLS), then put a vastly unqualified January 6th hack in her place.

I also wrote about what I deemed “Uncertainty Season,” doing economics 101-level analysis of pointing to the Michigan Consumer Sentiment survey sitting at historically recessionary levels and saying, “seems bad.” I wrote “When businesses face uncertainty, they typically pull back on their investments,” which is what we saw in the second quarter GDP weak business investment figures, as well as the tepid jobs reports all summer. Elon was the biggest thing I got wrong in that column aside from demonstrating how difficult timing the market is, as I wrongly assumed his government destruction would be more harmful to the basic components of GDP, whereas business investment is the main concern so far this year.

So now that the trade war has advanced much further from where it was in February and Musk is marginalized while the market seems to be souring on AI to some degree, there is a more concrete outline of an economic shitshow emerging through the haze. It’s time to write a more detailed update to my “I am become Cassandra” doomer bias which believes that we are living through the seeding of the next great economic crisis.

Stocks Look Tired

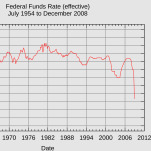

If you say the term “RSI” in a room of traders, you will spark hours of derisive argument, and this basic technical indicator for market momentum is useful on longer timeframes, but like every indicator, inherently flawed to a degree. Still, it’s a finance 101 tool to welcome newbies into the exciting world of studying line make boing, and generally speaking, the longer timeframe you measure something over, the larger the sample and better the data. RSI is useless on a five-minute chart, but on a monthly chart? There is something valuable in there, it’s just on the analyst to find it.

And every single monthly chart of every major index right now is painting what is called a bearish divergence spanning over several months, where the price line continues to make boing, but the RSI line does not make boing. Again, this is not conclusive, but price and momentum moving in opposite directions suggests declining momentum for the current rally, and when it painted this kind of bearish divergence between price and RSI in 2021, the market eventually tanked, as I showed in these zoomed out charts of the S&P 500, Nasdaq 100, Dow Jones and Bitcoin which all look remarkably similar to each other.

But you know, weekly timeframes are still pretty short for serious market folk, so let’s scale it up to a longer one in the monthly, maybe it’s not so…

fuck

— Jacob Weindling (@jakeweindling.bsky.social) August 19, 2025 at 11:22 AM

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-